The implementation of the Goods and Services Tax (GST) in 2017 is widely evaluated through the lens of fiscal policy and revenue mobilization. As an admirer of the law, framework, and its implementation (with some caveats), its long-term structural contribution lies in the substantial refinement of India’s macroeconomic data architecture. By replacing a fragmented, state-level tax network with a digitized transactional ledger under the Goods and Services Tax Network (GSTN), India established a framework that provides near real-time visibility into the formal economy.

This integrated setup enhanced the reliability, depth, and structural integrity of national accounts. Furthermore, it compressed the timelines required to publish actionable high-frequency economic indicators, positioning India competitively on the global statistical stage.

Enhancing Data Integrity: Reducing Estimation Noise

In macroeconomics, a nation’s total output can never be perfectly computed in real time; at a scale as vast as India’s, macroeconomic data can only be estimated through statistical models. Because estimation is inevitable, the structural integrity of the final figures depends entirely on the quality of the raw source data and the precision of the data-capturing process. If the primary data collection points are fragmented or prone to manual lag, the resulting national estimates inherit a compounding margin of error.

For those in the know, will recognize that historically, tracking Indian national account statistics faced structural hurdles due to the vast informal economy and fragmented tax administrations. National methodologies heavily relied on lagging proxy indicators, corporate sample frameworks, and periodic survey rounds to estimate quarterly production and consumption values.

The implementation of the GST architecture directly addresses this structural limitation by replacing disparate, lagging data streams with a standardized digital collection point at the transaction level. The unified digital architecture of the GST setup resolved several data integrity challenges through three specific mechanisms:

1. Major Reduction in GVA Estimation Noise

Gross Value Added (GVA), the metric for calculating GDP by the production method, requires isolating the actual value added at each stage of the supply chain. Under the pre-2017 regime, overlapping layers of central excise, service tax, state VAT, entry taxes, and local cesses were embedded invisibly within production costs. This cascading effect created systemic estimation noise (or cumulative errors, in common man’s language), making it near impossible to mathematically separate genuine value addition from tax compounding.

GST’s continuous Input Tax Credit (ITC) mechanism requires businesses to systematically declare both input purchases and output sales to unlock credits. According to studies on the formalization effects of the regime, this clean data flow allows the Ministry of Statistics and Programme Implementation (MOSPI) to trace the precise transactional footprint across industries, yielding a highly verifiable baseline for sector-wise GVA calculations.

2. Statistical Mapping of the Formalizing Economy

A significant portion of India’s legacy economic output resided in the unorganized shadow sector, traditionally estimated using periodic sample surveys (such as National Sample Survey Office rounds). The design of the GST framework institutionalized formalization. To preserve credit chains, registered enterprises required their smaller vendors to document transactions through the portal.

As the active tax base expanded from an initial 66.5 lakh taxpayers to over 1.6 crore registered entities (per GSTN and Press Information Bureau data), vast volumes of economic activity transitioned directly into the documented, auditable national accounting baseline. This shift drastically reduced the statistical error margins associated with estimating unorganized economic contributions.

3. High-Granularity Consumption and Trade Footprints

Because GST operates as a destination-based consumption tax, the system automatically logs the exact destination of taxable value. Combined with mandatory Harmonised System of Nomenclature (HSN) codes and the Integrated GST (IGST) framework, the system generates clean, cross-border transactional maps. Economists can now analyze exactly where value is produced versus where it is consumed, a metric that was largely an analytical blind spot under the previous state-siloed tax regimes.

Compressing Macroeconomic Publication Timelines

Beyond strengthening data accuracy, the digitized transaction trail solved the issue of administrative data lag. Before 2017, consolidating indirect tax data from disparate central departments and state treasuries took months, leaving policy makers dependent on backward-looking data.

The centralized architecture significantly contracted the publication timelines for core leading indicators :-

Logistical and Trade Velocity (E-Way Bills & E-Invoices): Prior to the reform, tracking inter-state trade volumes relied on manual registers from physical border check-posts. Consolidating these registers across states carried a 60 to 90-day lag. Today, because e-way bills and e-invoices are logged instantaneously, aggregate national logistical trade velocity metrics are processed and published within 24 to 48 hours of a month’s conclusion.

Immediate Consumption Proxies: Traditional manufacturing and consumption metrics like the Index of Industrial Production (IIP) rely on factory survey forms, maintaining a 6 to 8-week regulatory processing lag. Conversely, granular GST collection data and sector-specific tax filings are released on the 1st day of every single month – a mere 12-hour lag from the midnight closing of the previous month. This serves as a highly reliable, real-time proxy indicator for broader industrial momentum.

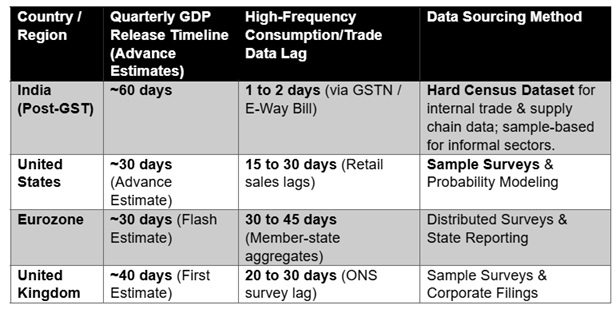

Quarterly GDP Timelines: Assisted by the rapid convergence of corporate tax aggregates on a single dashboard, India steadily stabilized its quarterly GDP advance release timeline to a reliable 60-day window (in line with MOSPI’s revised data series calendars), down from the highly variable 75-day lags seen in the pre-reform era.

Global Comparison: The Structural Advantage of Census Data

Following the deployment of this large-scale integrated digital infrastructure, India’s macroeconomic data release velocity has become highly competitive with advanced global economies:

Advanced economies like the United States and the Eurozone publish their initial advance flash estimates of quarterly GDP faster (within 30 days) due to deeply financialized markets, established corporate reporting cycles, and lower baseline volatility.

However, India maintains a distinct structural advantage regarding high-frequency internal trade and consumption data. Because Western nations lack a centralized, nationwide, real-time e-invoicing ledger, relying instead on distributed retail sales sample surveys, they cannot match India’s 48-hour turnaround time for publishing comprehensive supply-chain consumption metrics. The integrated setup of GST successfully converted an array of sample-based statistical guesswork into a hard, continuous transactional census for the formal economy.

The Foundation for Data Certainty

Ultimately, the structural evolution of the GST architecture has transformed India’s statistical landscape from a system of lagging, sample-based guesswork into a near real-time transactional census of the formal economy. By ensuring integration of national accounts, automated digital pipeline, the framework ensures that macroeconomic policy is guided by hard, high-velocity data rather than speculative projections. As this standardized ledger continues to mature, it provides the structural integrity and analytical precision required to confidently map India’s long-term economic trajectory.

G Saimukundhan is a Chartered Accountant.

Subscribe to our channels on WhatsApp, Telegram, Instagram and YouTube to get the best stories of the day delivered to you personally.