“World-beater in the making: UPI on the cusp of surpassing Visa’s daily transaction volume” – Screamed the title of an article in Moneycontrol. As I started the day with this wonderful news on UPI on the verge of becoming world’s largest digital payment interface, I could not help but marvel at this wonderful digital platform from India for the world, which has not just created another settlement mechanism, but has brought about revolutionary and transformative changes to the way in which people transact, and forcing the world to look at this new jewel from India’s digital prowess.

The Unified Payments Interface (UPI), launched in 2016 by the National Payments Corporation of India (NPCI), has transitioned from a niche digital payment method to the backbone of India’s financial ecosystem. With its unprecedented adoption rates, it has not just streamlined transactions, it has also emerged as a transformative force, driving formalisation, enhancing credit access, revolutionising settlements, democratising digital payments, and significantly contributing to the nation’s economic growth. It is not just a payment system. It is a pinnacle of indigenous innovation, emblematic of India’s ongoing digital revolution.

The Digital Revolution And India’s Technological Prowess

Our country has been undergoing a profound digital transformation, structured around what is known as the “India Stack” i.e. our own unique Digital Public Infrastructure (DPI). With its open-architecture approach, comprising foundational digital identity (Aadhaar), real-time payments (UPI), and secure data-sharing frameworks (DigiLocker, Account Aggregator), the “India Stack” has created a powerful ecosystem for innovation and public service delivery. No country has seen the sheer scale and speed of this transformation, making our Country a global leader in digital governance.

UPI is arguably the crown jewel of India Stack, showcasing the our nation’s capacity for designing and deploying cutting-edge technology at a population scale. It embodies India’s commitment to building public digital goods that are interoperable, inclusive, and cost-effective. Its success has garnered global recognition as a leading example of DPI, with several countries now looking to emulate its model to build their own real-time payment systems. This reflects India’s growing influence as a thought leader in digital governance and financial technology.

Formalisation Of The Economy Across Sectors

Traditionally, a significant portion of transactions, particularly in the informal sector and among Micro, Small, and Medium Enterprises (MSMEs), relied heavily on cash. This cash-based economy often operated outside the tax net, hindering transparency and accurate economic data collection, leading to stunted growth, both at an entrepreneur level and also at the country level. One of UPI’s most profound impacts has been its role in bringing large swathes of the Indian economy into the formal fold.

UPI has fundamentally altered this landscape by enabling seamless digital payments for everything from a street vendor’s tea and snacks to a small business’s supplies. The digital footprint facilitates better record-keeping for businesses, making it easier for them to comply with tax regulations like GST. Studies have shown a significant positive correlation between increased UPI adoption and higher tax revenues, with some research indicating a rise in GST filings among SMEs that adopted UPI. This formalisation improves financial governance, broadens the tax base, and allows for more effective data-driven policymaking.

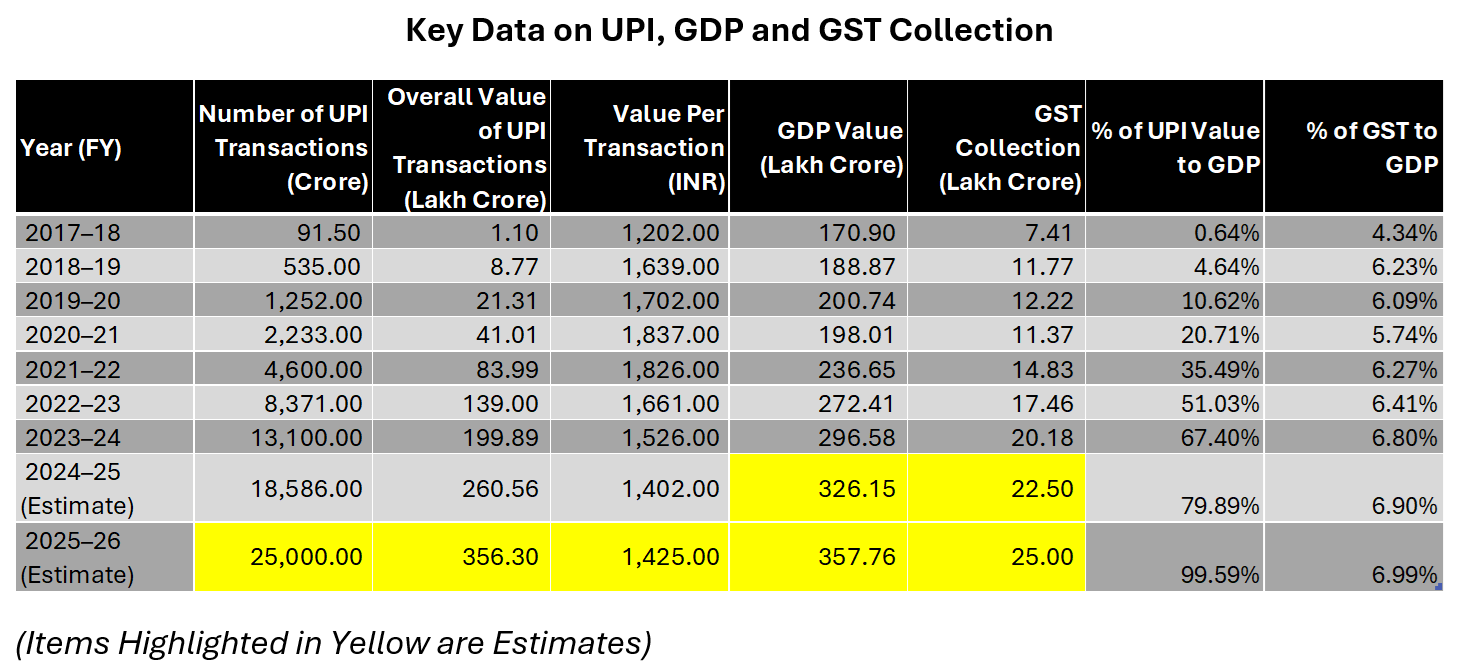

A good example of the formalisation is the ratio of the value of UPI transactions to the country’s GDP. Over the years, this has grown from less than 1% to almost 80% in FY 25, and expected to breach 100% in the years to come.

Enhancing Access To Credit

For millions of Indians, particularly small entrepreneurs, informal workers, and those in rural areas, access to formal credit has long been a significant barrier. The absence of a verifiable transaction history or a credit score often relegated them to high-interest informal lending channels, which comes with its own set of inefficiencies and baggages in the form of high interest cost, exploitative practices and rampant corruption. UPI is now changing this paradigm.

The real-time transaction data generated by UPI offers lenders valuable insights to assess creditworthiness more accurately and offer “sachet-sized” loans or small credit lines directly on UPI. The introduction of “Credit Line on UPI” by NPCI is a game-changer, allowing banks to extend real-time, low-interest credit to underserved segments who may not qualify for traditional credit cards. This innovation is crucial for financial inclusion, empowering individuals and small businesses to access formal credit, manage cash flow, and invest in their growth, ultimately fostering a healthier credit ecosystem.

Quicker And Cheaper Settlement

Prior to UPI, digital payment methods often involved multiple intermediaries, leading to higher transaction costs and delays in settlement. UPI, built on an Immediate Payment Service (IMPS) architecture, offers instant, 24/7, peer-to-peer (P2P) and person-to-merchant (P2M) fund transfers.

For businesses, especially small and medium-sized enterprises, this means immediate access to funds. This quicker settlement significantly improves cash flow management, reducing the need for working capital and enabling faster reinvestment. For consumers, the convenience of instant payments has eliminated waiting times and reduced dependency on physical cash. Moreover, UPI transactions are typically free for consumers and involve minimal or no charges for merchants, making it a highly cost-effective payment solution compared to traditional payment gateways or cash handling costs. This efficiency and cost-effectiveness benefit both individuals and businesses, reducing friction in economic activities.

Digital Transactions Made Size Agnostic

One of UPI’s most remarkable achievements is its ability to facilitate transactions across the spectrum of value, from micro-payments to larger sums, making digital payments truly “size agnostic.” Whether it’s a ₹10 payment for vegetables or a ₹1,00,000 payment for goods, UPI handles it with equal ease and efficiency.

This versatility has democratized digital payments, reaching beyond urban centers and tech-savvy users to embrace street vendors, small kirana stores, and consumers in remote villages. The simple QR code scan has become ubiquitous, transcending literacy and technological barriers. This broad applicability ensures that every transaction, regardless of its value, contributes to the digital economy, fostering a unified payment infrastructure that benefits all participants.

The volume of UPI transactions and its ratio to the Country’s GDP is a testament to the Indian consumer’s preference towards UPI. From just around 1 Lakh crore transactions in FY18 to almost 261 Lakh Crore transactions FY25, we are nudging towards 1 Lakh crore transactions per day. This is unprecedented for any country!

Catalysing Economic Growth

UPI’s multi-faceted benefits directly contribute to India’s overall economic growth. By formalising transactions, it expands the taxable base and improves the accuracy of economic data, leading to better fiscal planning. Enhanced access to credit, particularly for MSMEs, fuels entrepreneurship, investment, and job creation. The efficiency and cost-effectiveness of UPI payments reduce operational overheads for businesses, allowing them to focus on core activities and improve profitability.

The exponential growth in UPI transactions underscores a fundamental shift in consumer behavior towards digital payments, reducing the reliance on cash. RBI’s Annual Report for FY25 highlights that UPI transactions increased by 41.7% in volume and 30.3% in value compared to the previous fiscal, with UPI having the highest share (84%) in total retail payments, affirming its role as a key driver of economic activity. This strong performance contributes to India commanding a significant 48.5% share in global real-time payments by volume.

Conclusion

The Unified Payments Interface has not just facilitated digital payments; it has instigated a quiet revolution in India’s financial landscape. Its impact extends beyond mere transactional convenience, touching upon the very fabric of the Indian economy by formalising economic activities, unlocking access to credit, streamlining settlements, and democratising digital finance. As UPI continues to evolve and expand its global footprint, it remains a powerful testament to India’s digital prowess and a critical enabler of its journey towards a more inclusive, efficient, and robust economy.

G Saimukundhan is a Chartered Accountant.

Subscribe to our channels on Telegram, WhatsApp, and Instagram and get the best stories of the day delivered to you personally.