WTI crude oil price, benchmark for oil in America fell from $55 per barrel to -$37 per barrel. Anyone who purchased the contract stood to get both – oil & money. Which means, the person is getting paid to purchase oil! This leads us to a curious question – how fickle is the industry for prices to go negative? Let’s try to break the complexity of the oil industry for our understanding.

Oil – The Black Gold

Referred to as ‘Black Gold’, crude oil can vary in colour – black to yellow, depending on its hydrocarbon composition. Though crude oil was first discovered and developed during the Industrial Revolution in the 19th century, it was only when the first commercial well at Spindletop, Texas in 1901 was drilled, that modern oil era with large scale production was born. Mobility revolution in the 20th century propelled the oil industry to its zenith. Despite oil’s utility for various products, transportation consumption remains one of the most essential ones.

The Major Players

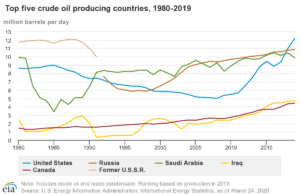

Though around 100 countries produce crude oil (unrefined petroleum), 5 countries account for about half the world production currently.

![]()

OPEC members (13 countries) produce roughly 40% of the world crude oil. Within OPEC, Saudi Arabia remains the most dominant member, being the largest oil producer. OPEC+, an amalgamation of OPEC and non-OPEC members like Russia, Mexico and Kazakhstan controls over 50% or half of the global oil supplies. Some of the top oil producing nations such as USA, Canada and China are not a part of OPEC. Despite being the largest oil producing country in the world, USA tends to consume most of it domestically. Similarly, most non-OPEC countries consume their produce internally or have to import despite producing oil. These dynamics render the non-OPEC countries ineffective in influencing the global oil prices.

Pricing is dependent on many factors – origin, extraction, transportation methods etc. Based on these factors, buyers and traders of oil need a benchmark to arrive at the value of oil. Through there are over a dozen benchmarks, the three primary ones are – Brent, WTI and Dubai/Oman.

Brent Crude – The most widely used benchmark, Brent is based on oil extracted from British and Norwegian fields in North Sea. Since the production is waterborne, it is easier and cheaper to transport through seas. This serves as a reference to more than 60% of global crude oil sales. It is primarily used in Europe, Africa, the Mediterranean, Australia and some Asian countries.

- Western Texas Intermediate (WTI) – This refers to the oil extracted from the wells in US and traded at Cushing, Oklahoma. Unlike Brent, which is based on offshore productions and seaborne deliveries, WTI is a market physically based on pipeline connections.

- Dubai / Oman (Middle East crude) – This benchmark is the average of the price of Dubai / Oman crudes. This is used for pricing of oil coming from Persian Gulf and Middle East.

- Overall, while Brent remains the reference for 2/3rd of the oil traded around the world, WTI is the dominant benchmark in US and Dubai/Oman remains influential in the Asian markets.

How Are Oil Prices Determined?

Supply and demand – the most basic of economic theories states that if supply goes up – prices tend to come down, if the demand goes up – prices tend to go up. Which leads us to the question – what disrupts the supply and demand thus affecting the pricing? Factors are many, some of them being:

- Cartels – The Oil world is divided into OPEC+ and non-OPEC+ countries. Founded in 1960’s one of the implicit functions of OPEC was to fix oil prices. They did it by controlling the supply tap. By squeezing the production, they forced the oil prices to rise and enjoyed greater profits. This modus operandi lasted through the 70’s and 80’s. USA, Canada, China and other non-OPEC+ countries tend to balance this skew.

- Geopolitical turmoil – Much of the crude oil productions regions are situated in countries historically prone to political upheaval. This volatility tends to affect the pricing arbitrarily. Events like the Arab Oil Embargo (1973-74), Iranian Revolution (1970’s), Iran-Iraq war (1980s), Persian Gulf War (1990’s), Asian financial crisis, all have aided in the price fluctuations.

- Environmental factors – Weather and climate changes tend to have to short but significant impacts. E.g. Hurricanes in Gulf of Mexico could affect the production and refineries in Gulf. As oil supplies from Gulf drop, the prices of the oil from USA may increase.

- Oil market transactions – Crude oil is traded in futures markets. Futures contracts can be a way to deal and shield from the unpredictability of oil prices. An oil futures contract is a binding agreement which gives the right to purchase oil at a predefined rate on a predefined price in future, irrespective the trading rate on that date.

What Led To The Fall?

Certain geopolitical factors combined with unprecedented lockdown measures in many countries due to Covid-19, led to reduction in global demand thereby affecting the price so much so that oil futures traded in negative.

- Bombing of Saudi Aramco (a Saudi Arabian multinational petroleum and natural gas company) halted half its capacity production temporarily in September, 2019.

- In January 2020, USA’s targeted killing of Iranian General Qasem Soleimani affected the stock futures and global energy prices. Iran is an energy superpower and contributes to over 5% of world crude oil production. The incident did create some flutter in the oil markets.

- Covid-19 pandemic set off a chain of reactions – Oil prices fell sharply owing to decreased demand (mostly in China) prompting OPEC members – Saudi Arabia & Russia to cut back on production to stabilise the prices. Initially agreeing to the cuts, Russia backed out of the agreement. Rapid growth of the US Shale industry and the previous energy sanctions by US on Russia seemed to play in the mind of President Putin. Reduced production by Russia and Saudi Arabia would mean handing over market share to US producers, which the Russians were unwilling to. Following Russia’s backing out, Saudi Arabia launched a price war in April by reducing its official selling price (from $14 to $8) and drastically increased the production.

A truce in OPEC finally led to Saudi Arabia cutting back productions drastically. But the wheels were already set in motion. Despite the oil producers scaling back the production, the global demand of oil had flattened owing to the unprecedented lockdown measures across many countries during the Covid-19 pandemic.

Supply reduced, but demand reduced very drastically, prices fell down, buyers were unable to purchase at low prices as storage capacities were full – in a nutshell, that’s how the oil futures nosedived!

Eventually, Covid-19 outwitted all the complexities of the oil industry and temporarily rendered the 3 major oil producing countries helpless – the USA, Saudi Arabia and Russia!